Bloom brings credit scoring to the blockchain. Founded Stanford engineers, Bloom makes credit global and inclusive. Bloom allows both traditional and digital currency lenders to serve billions of people who currently cannot obtain a bank account or credit score. Joey Krug (Augur / Pantera) and Joe Urgo (District0x) serve as advisors.

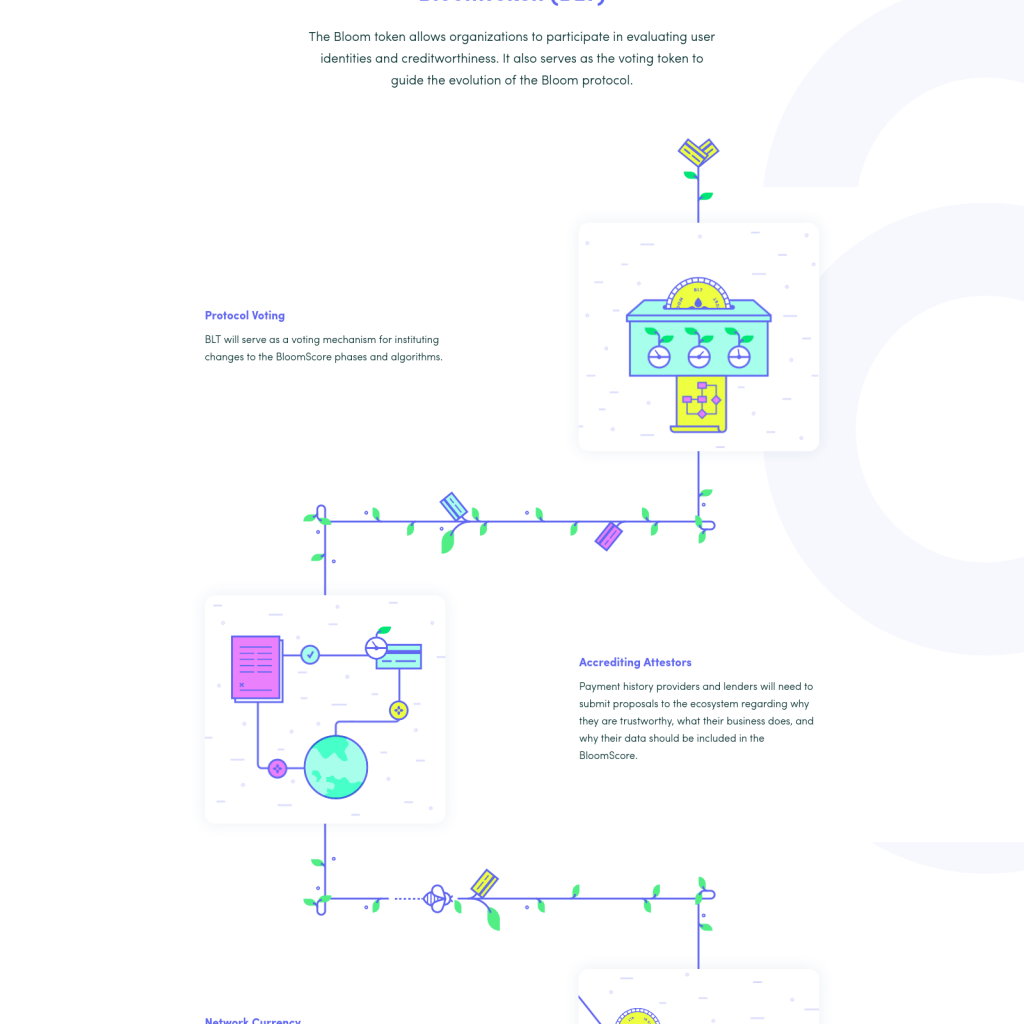

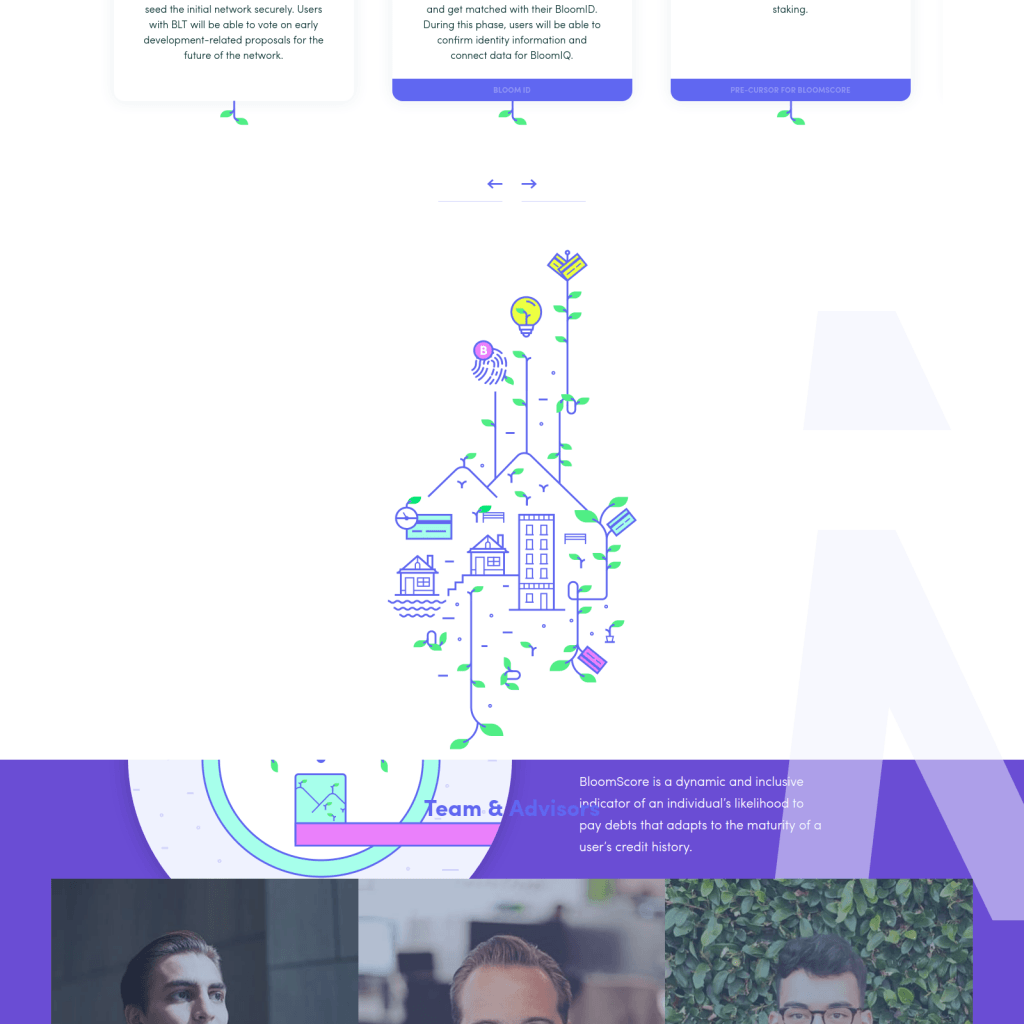

Phase 1 will allow for users to use BLT to invite their friends and colleagues to seed the initial network securely. Users with BLT will be able to vote on early development-related proposals for the future of the network.

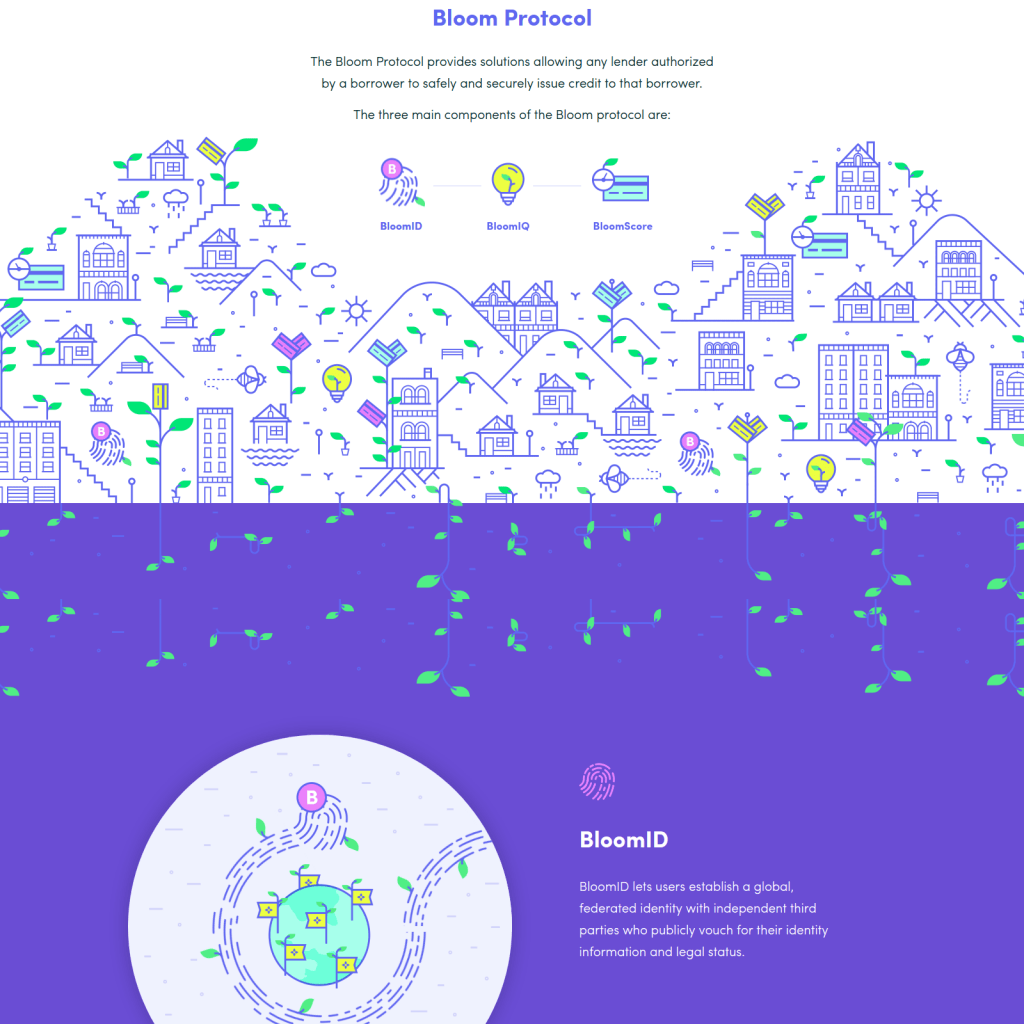

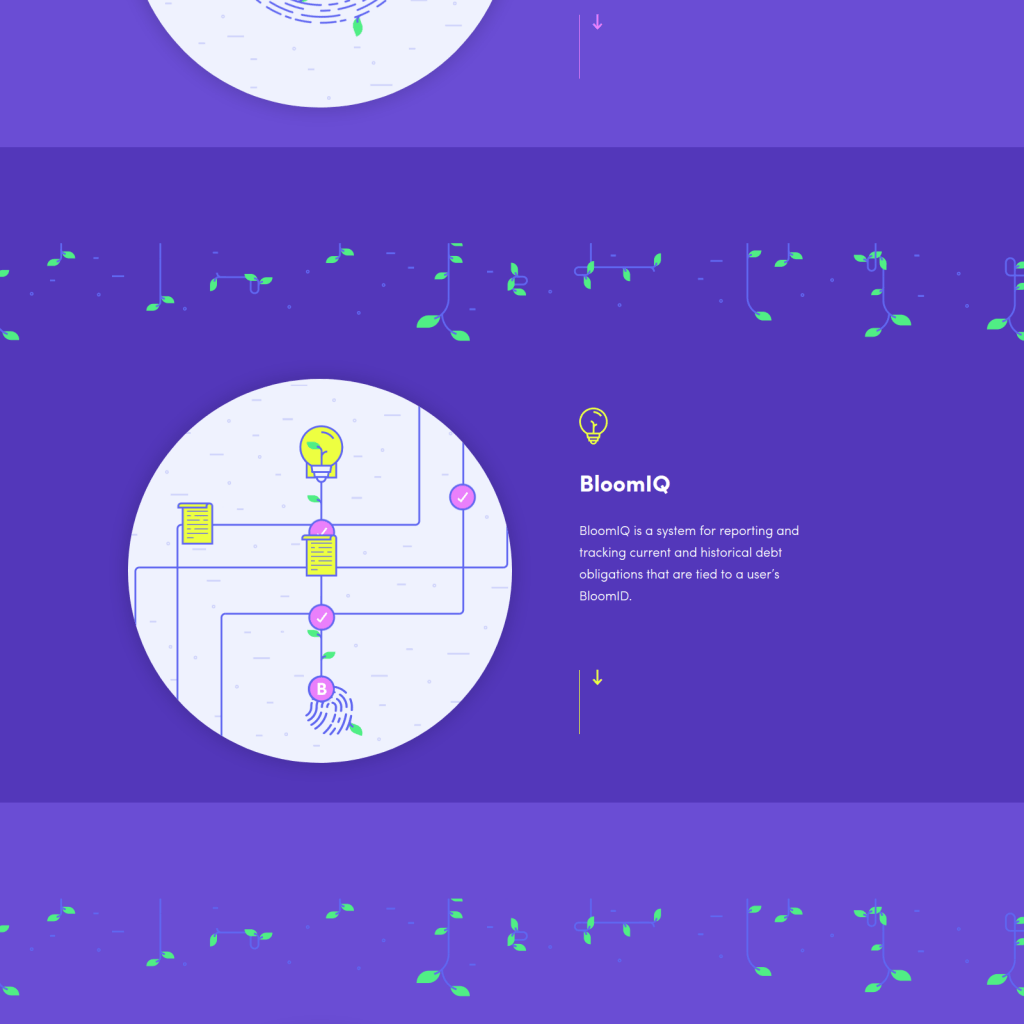

Phase 2: Bloom Identity Matching (BloomID)

Phase 2 will deploy an application allowing users to verify their identity and get matched with their BloomID. During this phase, users will be able to confirm identity information as well as add additional information which will be reflected in their score.

Phase 3: Credit Staking (Precursor to BloomScore)

Peer to Peer staking modules will be built first, followed by organizational staking.<br />

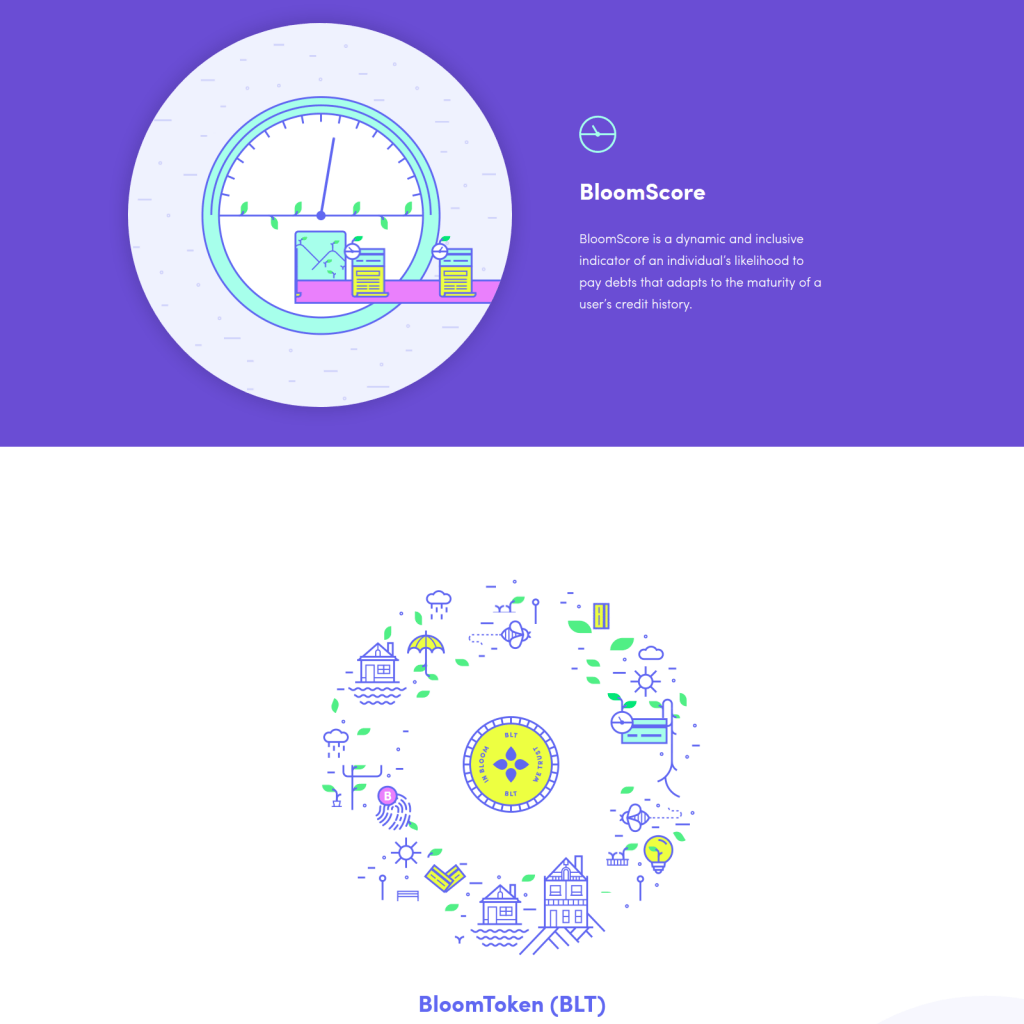

Phase 4: Creditworthiness Assessment (BloomScore)

Phase 4 will allow users to check their score, as well as open up a developer ecosystem for additional decentralized lenders to check a given user’s BloomScore, providing sufficient privileges are granted from the loan recipient.

Phase 5: Bloom Credit Protocol Launch + BloomCard

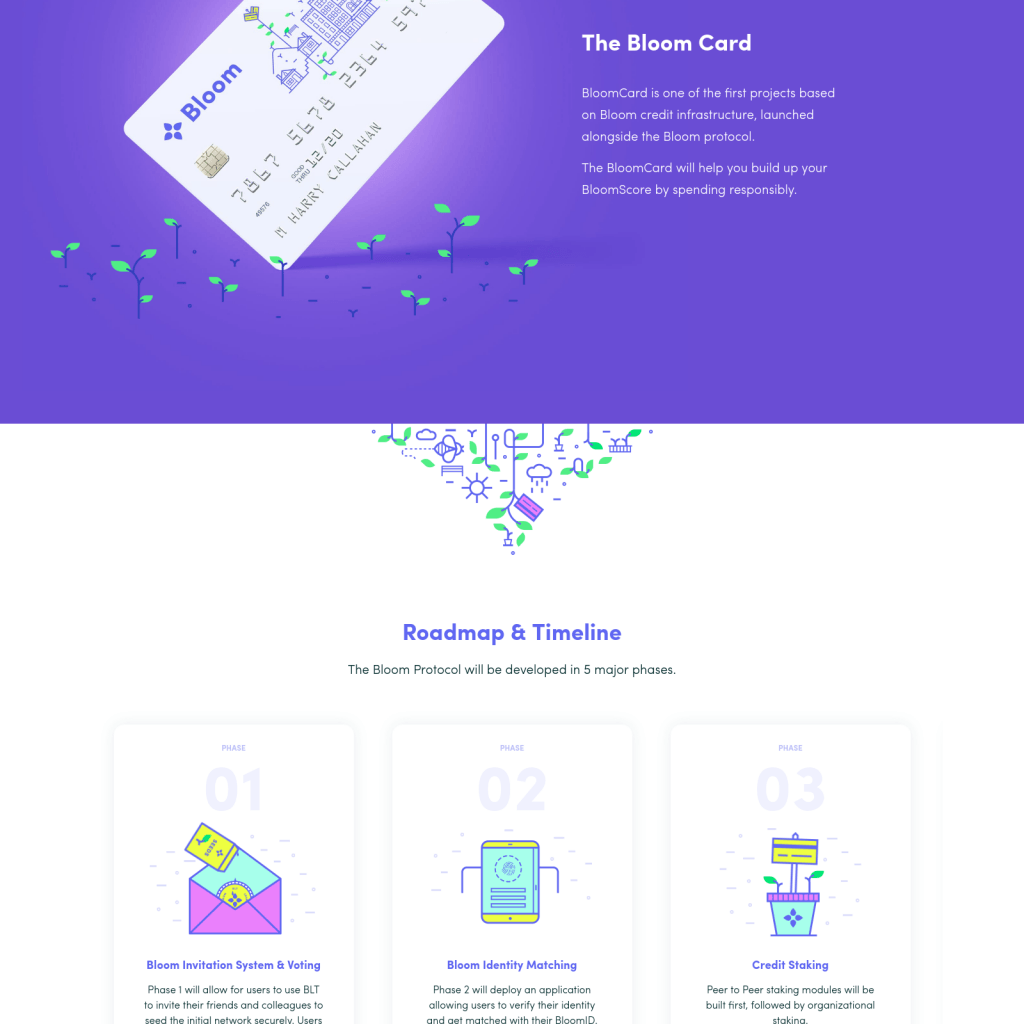

Once the risk assessment and scoring protocol is complete, Bloom will launch the BloomCard. The BloomCard will serve as the first full credit card on the blockchain, offering credit services to the nearly three billion individuals who are currently not able to participate in the global credit ecosystem.

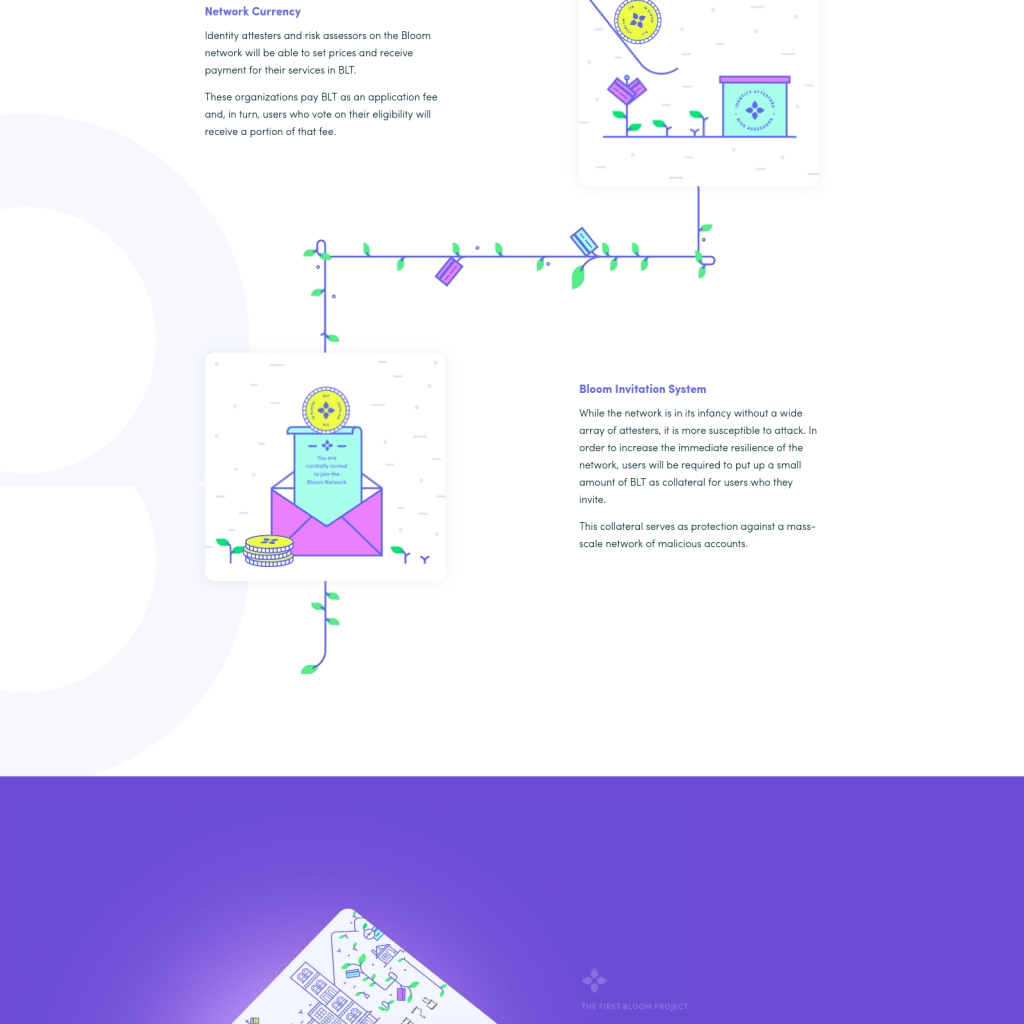

BLT flows through the network. Lenders, data attestation providers, and borrowers all own Bloom Token and their amount acquired will correlate to their influence on the network. As a result, there is an even distribution of BLT relative to a given player’s influence in the ecosystem. Assigning the ability to propose and vote on scoring-level improvements and accrediting actors within the network to these tokens creates a fair and democratized setup.

.png)